Post-Mortems, Part 1

With this blog, I'm trying to really sink my teeth into the whole "all I want to know is where I'm going to die so I never go there" idea promulgated by Munger. Investing in public equities has been such a favourable endeavor historically, that as long as you can cut down on mistakes and survive, you'll do extremely well.

A large percentage of professionals with good track records seem to hit roadblocks and are eventually unable to sustain good or even reasonable performance at some point. There are both macro (regime change) and micro reasons (a bad stock pick) for this.

There are so many examples to learn from. I like studying them because I can deconstruct errors in judgement others made and learn on their dime.

You can't go overboard in learning from past mistakes or investments results. Each individual situation is different and what did not work for one person may end up working for another person or working well in a different time.

Nonetheless, I do think diving deep into past case studies helps me think about what kinds of mistakes are common and why they happened. It's never enough and you have to go beyond heuristics and patterns and look for exceptions to the rule in investing, but it is a starting point in trying to avoid or at least minimize similar mistakes myself.

Post-Mortems:

Bob Goldfarb / Valeant:

At the peak in mid 2015, Valeant was one quarter of the Sequoia mutual fund portfolio of ~ 7.5B dollars. Today, Sequoia has an AUM of half that, and Mr. Goldfarb is no longer there, leaving after the Valeant crisis. Sequoia is trailing the S&P 500 over the last 5 and 10 years.

What is funny is I can only find annual reports and annual meeting transcripts on their website starting from 2016...hmm.

Anyway, though the company is now so hated that it angers some people when I say otherwise, Valeant started as a reasonable idea. (ha 75% of people have stopped reading further) There was a Canadian pharmaceutical company named Paladin that pretty much followed the early Valeant model to a T and did extremely well (~26% CAGR over 17 years until its sale in 2013).

They thought pharma R&D was unpredictable and low return. Innovation was also often taking place outside of the Big Pharma ecosystem and the industry had to go out and spend billions on budding biotech companies to refill patent portfolios due to constant patent cliffs.

Paladin's strategy was:

1) to focus on low volume products in very niche categories that would be ignored by Big Pharma and that could survive ignored even post patent expiration

2) focus on quasi-consumer products in pharmaceutical areas like skincare, topicals, aesthetics/cosmetics, where you're able to develop brand power that insulated products from patent cliffs

3) rather than expensive R&D, scour the world for interesting niche drugs that were already commercialized and use the company's expertise and distribution to get them approved and marketed in Canada. Often, the original manufacturer of the drug was a very small local company in Israel or Belgium or something that was happy to give Paladin the license to sell the product overseas as the company was too small to do it themselves and the product was too low volume to have Big Pharma interested in paying a licensing fee and expanding its distribution.

Also, the CEO was a 2nd generation pharma executive, whose father/family owned 30% of the firm. He executed with a long term mindset and a healthy balance sheet. Paladin followed the above strategy for almost 2 decades, doing small tuck-ins and adding licenses here and there, doing really well over time and eventually selling the company for ~$1.3B.

But as you can see, this strategy was pretty much about hiding from Big Pharma and picking out little niches where you could get riches. Niches get riches.

You can't build a 100B company that way and that unending ambitiousness of management is when Valeant went from a decent idea to a really bad idea and even a dangerous idea that forced all those bad incentives which of course brought the company down.

Sequoia was very early into Valeant, investing in 2010. They were attracted by the reasonable ideas Pearson had early on, saw him execute on them and grow the company, and saw enormous stock price gains right away. Well, at that point, Valeant CEO Mike Pearson started to get deified basically. You start to believe the CEO more than you believe yourself because he has made you so so much money so quickly.

The whole Valeant situation reminded me of a famous reply a Sequoia PM gave to a fundholder one meeting about why they held such a large stake in Fastenal, which seemed very overvalued. The PM responded that no matter how they did their math, they couldn't exactly make the Fastenal valuation work, but the management team was so so good that they just didn't want to sell.

(which by the way turned out to be the right decision! - I have no easy answers lol, investing is not that simple)

Back to Valeant. I think around late 2012/early 2013, Valeant started to realize that a niche type strategy was only going to take them so far and started to ratchet up the aggressiveness. Management was paid based on large options grants that actually multiplied 2x or 3x based on total shareholder returns. ValueAct essentially designed the policy and it incentivized extremely aggressive behaviour.

If you make us 10%/yr over the next 3 years, you get x # of options, if you make us 20% you get 2x and if you make 30% you get 3x...well, surprise, surprise.

So, late 2012/early 2013. That's when Philidor was formed. That's when the prices for drugs for rare diseases that old ladies used to stay alive started tripling in price. That's when they started buying lower quality assets. It was at that point a completely different idea than the reasonable idea at the start.

Sequoia even knew that they weren't following the strategy anymore!! I go back to the comment earlier that when the CEO executes and makes you a lot of money, you start to believe the CEO's words more than your own eyes.

Here, from their 2015 annual report, is what Sequoia said their research told them:

I seem to recall also in one of their Q&As, a Sequoia analyst repeated that it was a bit head-scratching that Valeant paid so much money for Salix when it seemed their main product would hit a patent cliff pretty soon.

In early 2015, Valeant also bought Sprout Pharma from a woman in a pink suit. This company was working on a female Viagra, though there was no product as of yet. Valeant felt only $1B for the chance to own a possible female Viagra, well damn that seemed like a pretty good deal.

What happened to Valeant's criticism of Big Pharma constantly overpaying for vaporware R&D IP??

(Valeant basically gave back Sprout to the former shareholders for next to nothing in 2017)

So, anyway, here is my assessment of what happened at Valeant. A new CEO took over and said some pretty intelligent things about the state of the industry. Sequoia bought in. He executed seemingly quite well, usually buying a bunch of skin care or cosmetics type drugs and low valuations that were very geographically diversified and mostly unaffected by patent expirations. Then a very very aggressive options scheme was put in. The CEO realized, there's no way I can actually grow this company all that much bigger because my whole strategy is to stay small and hide in the crevices where Big Pharma does not compete. I have to get way more aggressive if I want to make my billions. (The bullshit spewed by management also had to go up by a factor of 10x to cloud the strategy change)

Sequoia had the analyst IQ and the research firepower to pretty much catch on to the change in strategy. (Though Philidor took everyone by surprise). But the CEO already made us so much money, ValueAct are on the BoD, we think he's a genius etc. We make heroes out of mortals in this business, sometimes deservedly but many times not.

They basically had the analysts that knew what was happening but they were under Pearson's spell. It would be hard not to be under his spell if you're up 10x in 5-6 years.

Investors give longer leashes to managers that have a history of making them money. But when the strategy changes, you can't rely so much on old records and faith. A much more benign example is when I hear people say they will give Comcast "the benefit of the doubt" in buying Sky because of their good capital allocation track record in the past. Comcast invested capital for decades into 1 industry, cable systems, and ran them well. In the midst of the financial crisis when everything was cheap, they bought a media business, NBC, from a forced seller and got a good result. In 2016, they did a tiny tuck-in deal with maybe 1/4 of one year's cash flow to buy Dreamworks Animation. (sample size = 2)

To equate that to a months long auction from which they came out with arguably the worst of the assets being bid for, paying top dollar, in an environment of greater than ever competition from new entrants...

It's a case of refusing to believe what your own eyes tell you, even while DirecTV and Dish bleed customers.

--

It's easy now for people to laugh at Valeant investors with hindsight but to a particular style of investor, Valeant was catnip. Munger talks about how you can probably work hard and you can become the best plumber in your small town or whatever but for those totally outlier success stories, you need a lollapalooza of 4 or 5 different factors to line up perfectly. In many ways, Valeant was a lollapalooza at being good at being a wolf in sheep's clothing. It's no wonder that many very solid investors with decades long, strong track records (ValueAct, Ackman, Greenberg, Sequoia, Giverny to name a few) ended up putting up to 20%-30% of their portfolios into it and suffering massive losses.

The concept that contributed to this that I want to touch on is mimicry. Aggressive mimicry is when a predatory species will mimic a harmless species, or a log or a bush or something. The little fishy swims towards the attractive bright light, which turns out to be a predator anglerfish. The other kind of interesting mimicry in nature is Batesian mimicry, where a harmless species resembles a harmful species in order to keep prey away, i.e. a non-poisonous frog has almost the same colour pattern as a poisonous frog.

I think management teams do this mimicry all the time! They study what we investors want to hear, because there are millions, if not billions of dollars at stake for them. Pearson asking Ackman for $20 bucks for the Chipotle burrito Ackman bought on Valeant's company money impressed him so so much, he recounted that story multiple times afterwards, ignoring the private jets and all that.

This guy Pearson is cheaper than 3G!

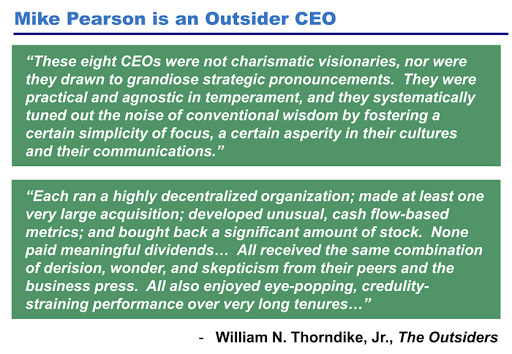

I truly believe that had that Outsiders book not just come out a few years before and imprinted into Buffett-following investors a certain model in their mind of what to look for, the Valeant ordeal could've played out differently.

Remember this presentation?

https://www.sec.gov/Archives/edgar/data/885590/000119312514152949/d714482d425.htm

I think Valeant was really really good at that kind of mimicry. There were 3 levels of mimicry there.

Valeant mgmt presented themselves as extremely cost conscious spartans bringing discipline to a fat, rich industry like pharma (3G - consumer staples).

He was Malone-like in his comfort with a highly levered FCF model (aka tons of debt), focus on almost no tax 'leakage' and a distaste for reporting GAAP earnings.

Lastly, there was the Outsiders/Buffett homage. It basically turned certain investors' brains into putty.

It is easy to meme certain examples of this mimicry. Like Holmes wearing Steve Jobsian black turtlenecks. Or people calling a possible drunkard, shaggy looking Pearson an 'Outsider'. But that's because that may not be your particular style of investing so that type of mimic won't entrap you. A cheetah can hide in the savanna grass and gain an advantage but if you moved that cheetah into the arctic and it had to compete with a polar bear, it would be toast.

If you were a VC that had worshipped great founders like Jobs your entire career and so did all of your colleagues, then Theranos would've been a different thing for you. If you spent your life reading about Buffett, read the Outsiders 3 times, bought Post Holdings just because Stiritz was mentioned in the book...then Valeant had a certain powerful effect on you.

Deep value investors or any other type of investors are not immune. There are many deep value people that hold Fairfax or hold Loews and have held for decades even though the track record for the last 20-25 years has been very poor. They hold because the CEO/controlling shareholders map on well to their own biases and say things they like to or want to hear (calling tech overvalued, saying the market is a bubble etc.). In this case, Watsa is genuine/ethical obviously, but many CEOs are not. They have gotten very good at using the right terms and mimicking whoever they'd like you to think they are.

--

"Everybody does it"

Sequoia 2015 Q&A:

This was a common idea at the time. US healthcare and drug pricing had been a certain way for so long. Everybody was jacking up prices. Sure, Valeant was a bit (or way) more aggressive but they weren't doing anything new.

The industry was raising prices at 4%-5% faster than inflation (on non-generic drugs). It's a mental leap to normalize 400%-500% annual price increases as par for the course. Nonetheless, the 'everybody else is doing it' idea has been the cause of many follies / errors of judgement and ethical lapses in the past and it will continue to be in the future.

The one question that I do wish was considered more rigorously was that if it was that easy, why didn't more pharma companies raise prices faster, and indeed, why didn't the sellers selling to Valeant just increase prices themselves and keep the extra profit?

This is what Sequoia had to say about that:

--

Summary of mistakes made:

1) When something goes up a lot, you feel more 'loyal' to it and you give a longer leash to the management team even if the strategy and capital allocation of the company has changed drastically. Sequoia invested early and made multiple times their money in just a few short years. The faith in Pearson and the related prospect of missing out on similarly strong future compounding made them unable to pare down the position even as their own analysts struggled to understand rationales for new deals Valeant was doing.

2) Management teams are great at mimicry (and investors are also often desperate to superimpose a Buffett or a Malone or a Diller on a CEO). To a degree, all we are doing in investing is trying to study past patterns of success and find replications today. The next Buffett, the next Malone, the next 3G (or as VC's say, the Uber of X) is an opportunity for good mimics to take advantage.

3) Viewing high hurdle but extremely aggressive stock compensation as always a good thing is simplistic, esp when rewarding short term stock performance. In the case of Valeant, it's probably the root cause of the demise.

4) Unethical and stupid practices can be explained away by saying "Well, everyone else is doing it."

5) On a personal note, I invested, at cost, about 13% of my capital into Valeant and lost about 8% of my capital in it eventually. I made all the above mental leaps and errors and mistakes. Another thing that happened too was that all my investment idols, so to speak, that I'd read about in books and newspapers were investing in this one single company, and betting big.

--

All of the above are simple heuristics or things that short circuit your brain into taking shortcuts and looking at a company from the perspective that someone else wants you to see, rather than with fresh eyes.

I do think I'll probably make some of these errors (hopefully in smaller ways) again in the future. Investing is grey, not black and white.

In overdosing on learning from past mistakes, you'll just make new ones.

For example, it's quite clear from reading technical, non-political government reports that Transdigm raises prices very aggressively on their products and has done so for decades. But they don't make life saving drugs for old ladies!

You have to try to go in with fresh eyes and a logical framework, instead of a dogmatic one.

However, the one thing all this did make me appreciate is how rare it should be for any business to become a 15%-20% of greater position in your portfolio. Valeant wouldn't have been nearly as memorable a story as it was for the investing community if the 4-5 major shareholders didn't put 15%, 20% sometimes 35% of their portfolios into the stock but had instead just invested 5% or 10%. IIRC, I'm pretty sure Giverny didn't FOMO as hard as many of the others only did put in about 5%.

I'm going to keep this post-mortem series going with another case study in Part 2. Part 2 will be on Bruce Berkowitz, a former Morningstar fund manager of the decade, who had more than $20B of AUM in his mutual fund at one point.

:)